By Blake Schraft, Director, Large Claims Business Development

Where an employer population resides has a substantial impact on the calculated stop-loss insurance premium rates. Why? The cost of providing medical care varies, sometimes dramatically, from region to region.

Since employer stop-loss insurance rates are a function of, and largely reflect the cost of care in a given region, employers with a concentration of employees in a more expensive state are going to pay a higher stop-loss insurance rate than an employer with a concentration of employees in lower cost states.

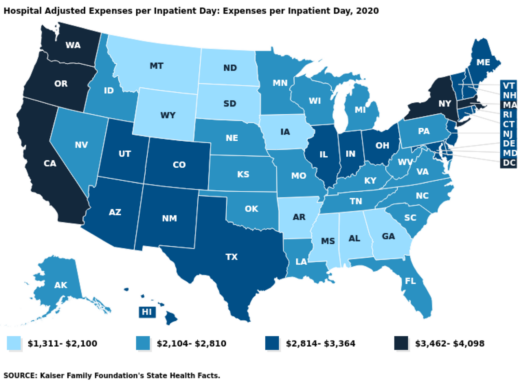

The map below illustrates how the cost of inpatient hospital care varies around the country. The average expenses per inpatient day in Alabama, for example, is 56% less than the expenses per inpatient day in California.

Stop-loss insurance carriers incorporate an ‘area adjustment’ into their stop-loss rate development process to accurately reflect the cost of care across the employer’s population base. The cost of care itself is a function of the billed charges assessed in a region, adjusted to reflect the discount(s) that are negotiated by the managed care network that is involved. This managed care network adjustment is based on market intelligence collected by industry organizations on the discounted cost of care in a given region (typically at the zip code level).

For these reasons, it is important for a stop-loss insurance carrier to receive an accurate census at the time of quoting and also know what managed care network will be utilized during the term of the stop loss policy.